Sustainable innovation efforts call for integrating two competing ways of thinking about a business.

Having worked with business leaders for years in the pursuit of innovation, I have come to realize that there is a fundamental reason companies fail to develop an innovation competency. At the simplest level, innovation becomes too closely aligned with looking toward the future and neglects the contribution of the organization’s historical knowledge base.

This isn’t obvious at first and takes a bit of explanation to bring it into focus. For me, I started coming around to the idea after reading Rodger Martin’s description of the two core competencies of every company. If you have the time and interest, it is worth reading his work (https://rogerlmartin.com/docs/default-source/Articles/business-design/rotman_winter_05_validity_vs_reliability ) because this blog post is just skimming the surface.

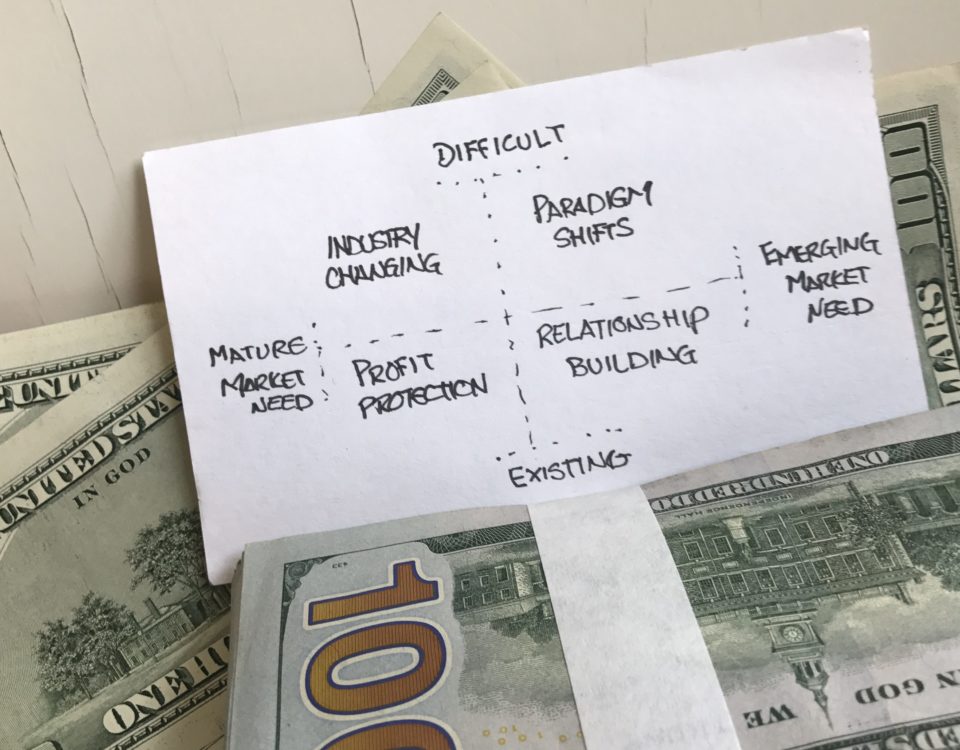

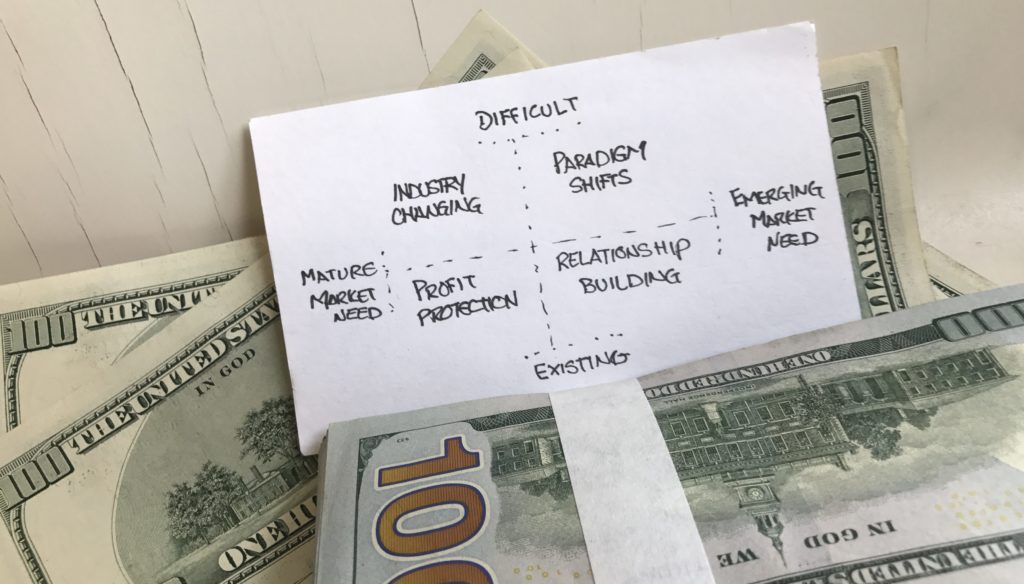

The model describes how growth-oriented companies have two modes of operation that often are viewed as incompatible. One mode focuses on the past and one focuses on the future, and the inability to integrate the two explains why companies find it so hard to innovate.

Established businesses are great at maintaining value through greater efficiency and effectiveness; but over time, these businesses become irrelevant. Start-ups are great at spotting unmet needs and driving a relentless charge — only to find that they have an unsustainable business model.

Innovative companies like Amazon find a way to do both, keeping an eye on the bottom line while sensing the hearts of their customers. The combination of these two capabilities is the key to innovation.

Is there a way for your company to innovate on a constant basis? Yes, and it involves integrating your past and future.

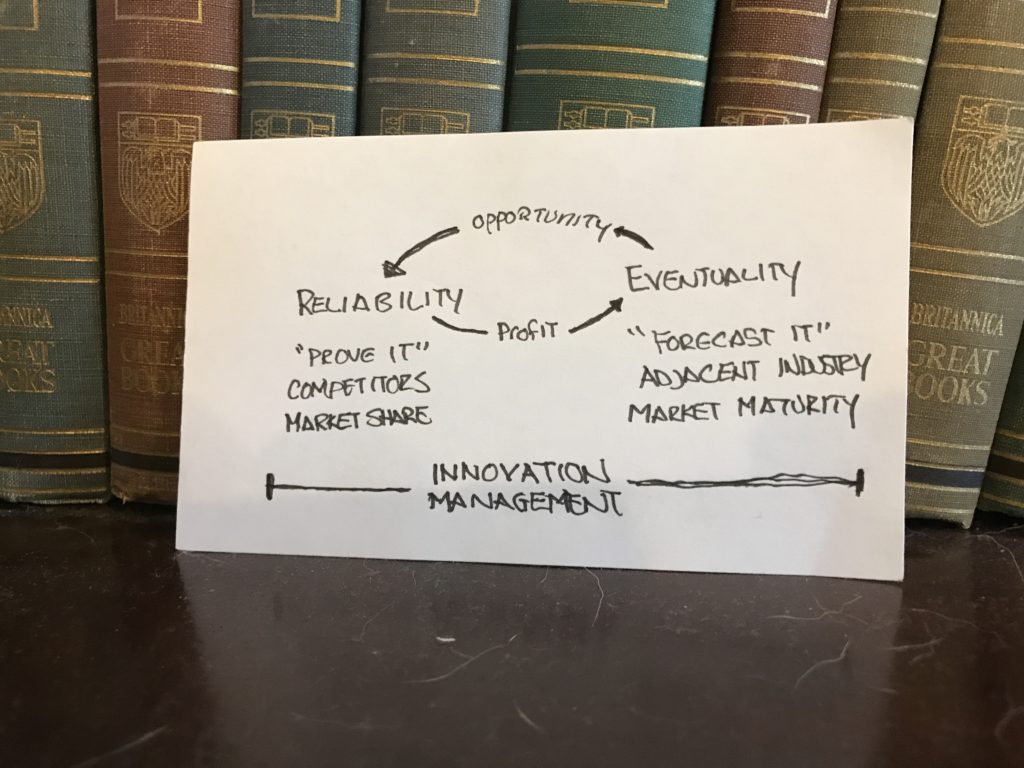

Your company most likely operates in “reliability mode” most of the time. Decisions are made by looking backward into the operations of the company and finding elements that lower costs or drive more revenue from existing operations. When the ROI for a project is positive (based on historical data), it gets funded. You know this mode dominates when you are asked to “prove it” before receiving funding.

Start-up companies operate in “eventuality mode.” It is the act of looking forward into the changing marketplace and finding an underserved, small and growing consumer segment that will disrupt the demand curve of your industry. Typically, companies don’t act until the disruption is obvious, and then the entire organization is directed to meet the trend with enough momentum to catch it. You know this mode dominates your company when you are asked to commit to a new vision.

When a company can integrate the two modes, and not rely too heavily on either of them, innovation succeeds. Here’s an example. One of our clients, a large health insurance provider, was unable to get approval to fund a customer-centric redesign of its member website. The reliability metrics (e.g., number of members using the site, call center inquiry reduction) couldn’t prove that a $10 million investment would pay off. Then health care reform created a well-defined “eventuality”; more people would be entering the market for individual health insurance and using digital channels to manage their claims. Once it became clear that the company’s core competency of managing member claims was at risk, the funds were allocated.

Your company might not be lucky enough to have a government-mandated eventuality looming over the horizon. As a leader, you have to put the time and effort in to provide a level of certainty about future events that can balance the natural focus on the reliable past. So before you claim that symptoms such as risk aversion, lack of ideas and data paralysis are the problem, evaluate how effectively you integrate capabilities of reliability and eventuality into your business decisions.

{kind=link}

1 Comment

https://shorturl.fm/szIJP